Australian Sportstech Sector Hits A$7.11 Billion Milestone as Global Momentum Accelerates

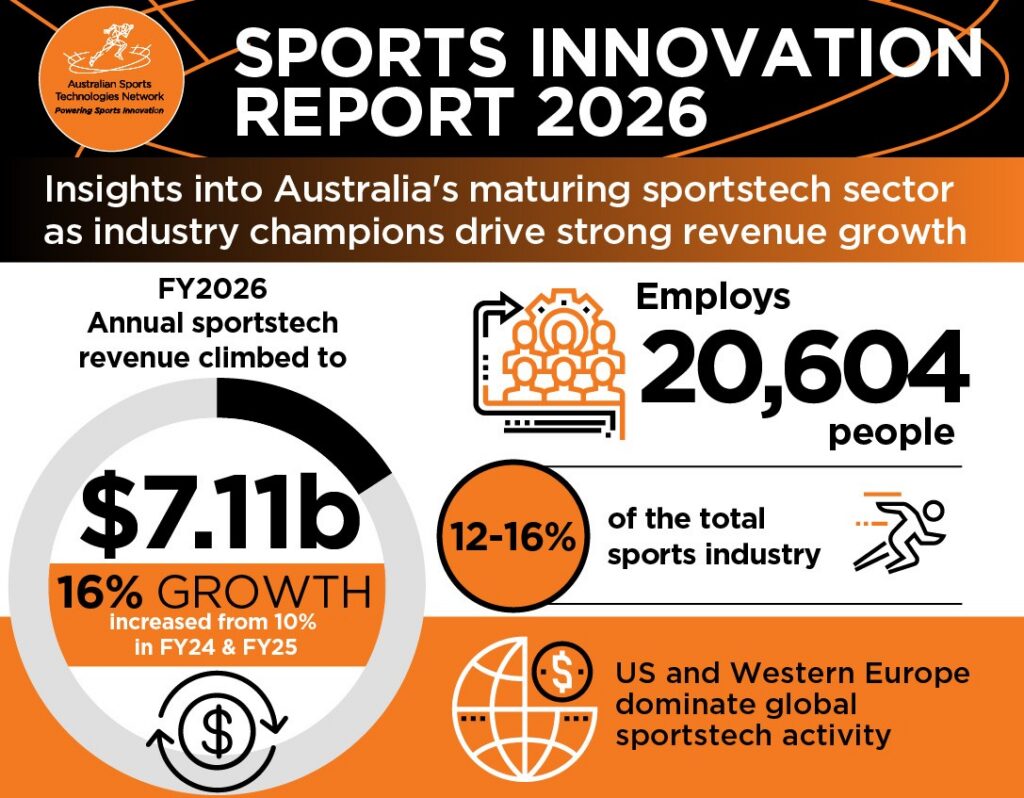

Australia’s sportstech sector has reported a period of acceleration, with annual revenue surging to $7.11 billion in FY2026.

According to the Australian Sports Technologies Network (ASTN) fifth annual Sports Innovation Report, the sector’s growth rate has climbed to 16 per cent, up from 10 per cent in the previous fiscal year. Alongside this financial expansion, the industry has seen a 6 per cent increase in employment, now supporting 20,604 roles across the country.

The census identifies 924 companies nationwide, with a significant concentration of market power held by a cohort of 115 high-performing businesses. These industry leaders are responsible for generating 89 per cent of the sector’s total revenue, or $6.30 billion, and 74 per cent of its total employment. Companies such as Catapult Sports, PMY Group, Bodd, VALD, and Champion Data are cited as primary drivers of this growth, successfully positioning themselves as both domestic market leaders and formidable competitors in global markets.

Noting that while the APAC region comprises only 10 per cent of global sportstech activity, Australia’s reputation as a specialised innovation hub is strengthening, ASTN chair, Dr Martin Schlegel, said: “Australia’s sportstech sector is experiencing sustained growth and reaching unprecedented momentum on the global stage.”

“We are seeing a growing number of fast-scaling companies emerge – companies that are successfully competing in global markets while building strong market positions at home,” Dr Schlegel said.

Despite this success, the report highlights a challenge: a growing tendency for Australian startups to adopt a “global-first” approach. Dr Schlegel explained that many startups struggle to secure early domestic traction due to difficulties engaging with local sporting organisations and corporates.

“Australia has the capability to be a leading testbed for sportstech innovation, yet many startups still struggle to secure early domestic traction.”

As a result, more companies are seeking validation and scaling overseas first, meaning Australia is often missing the opportunity to support and benefit from early-stage growth,” Dr Schlegel noted.

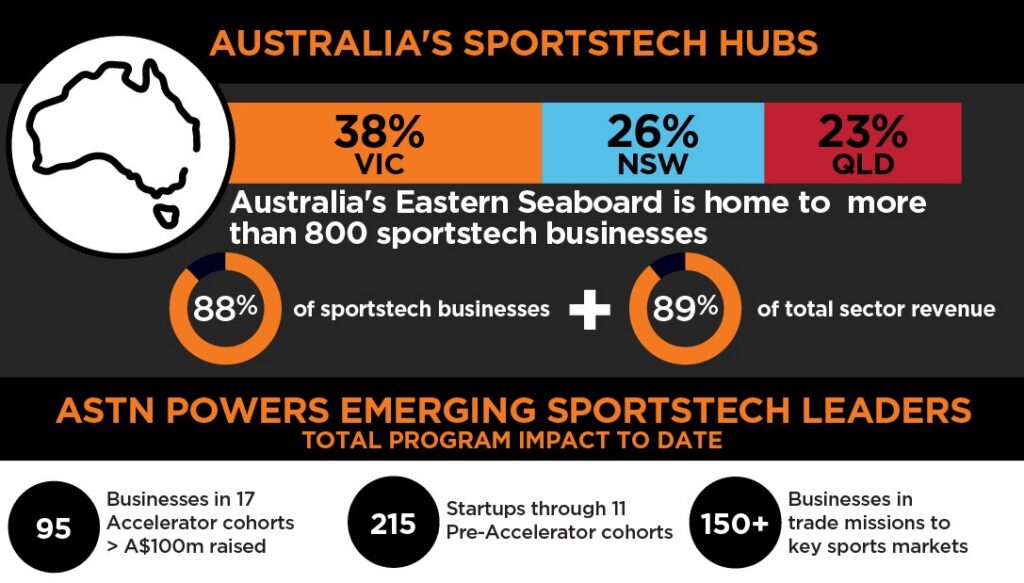

Geographically, the industry remains heavily concentrated along the eastern seaboard, with Victoria, New South Wales, and Queensland accounting for 88 per cent of all sportstech businesses.

Victoria continues to lead the national ecosystem, with Melbourne contributing 39 per cent of total sector revenue.

However, Queensland is rapidly rising as a key hub, supported by strategic investment ahead of the Brisbane 2032 Olympic Games, with forecasts suggesting it will overtake New South Wales in business numbers and employment by 2028.

Don’t miss out on the latest in sports business – Subscribe today to the free Ministry of Sport newsletter and stay ahead of the game. For even more exclusive insights, event tickets, professional development and networking events, become a MoS Member today!.

Latest News

Similar Stories

Philanthropist John Arnold Launches $2.6 Million Research Initiative into Evolving Sports Betting Landscape

John Arnold, the billionaire philanthropist and former energy trader, has committed USD2.6 million...

Sports analytics sector poised for massive expansion to $10 billion by 2030

The global sports analytics market is on a trajectory to reach USD9.64 billion...

The Economics of Wimbledon 2026: How a Two-Week Tournament Built a Half-Billion-Pound Machine

In an analysis piece by Daniel Pereira, he shares how Wimbledon’s century-old strategy...

It's free to join the team!

Join the most engaged community in the Sports Business World.

Get all the latest news, insights, data, education and event updates.